1. Introduction

It’s fairly clear that the majority of our work will probably be automated by AI sooner or later. This will probably be doable as a result of many researchers and professionals are working arduous to make their work accessible on-line. These contributions not solely assist us perceive elementary ideas but additionally refine AI fashions, finally liberating up time to give attention to different actions.

Nevertheless, there may be one idea that continues to be misunderstood, even amongst consultants. It’s spurious regression in time collection evaluation. This challenge arises when regression fashions counsel robust relationships between variables, even when none exist. It’s usually noticed in time collection regression equations that appear to have a excessive diploma of match — as indicated by a excessive R² (coefficient of a number of correlation) — however with an extraordinarily low Durbin-Watson statistic (d), signaling robust autocorrelation within the error phrases.

What is especially shocking is that the majority econometric textbooks warn in regards to the hazard of autocorrelated errors, but this challenge persists in lots of revealed papers. Granger and Newbold (1974) recognized a number of examples. For example, they discovered revealed equations with R² = 0.997 and the Durbin-Watson statistic (d) equal to 0.53. Probably the most excessive discovered is an equation with R² = 0.999 and d = 0.093.

It’s particularly problematic in economics and finance, the place many key variables exhibit autocorrelation or serial correlation between adjoining values, significantly if the sampling interval is small, reminiscent of every week or a month, resulting in deceptive conclusions if not dealt with appropriately. For instance, at the moment’s GDP is strongly correlated with the GDP of the earlier quarter. Our submit gives an in depth rationalization of the outcomes from Granger and Newbold (1974) and Python simulation (see part 7) replicating the important thing outcomes offered of their article.

Whether or not you’re an economist, information scientist, or analyst working with time collection information, understanding this challenge is essential to making sure your fashions produce significant outcomes.

To stroll you thru this paper, the following part will introduce the random stroll and the ARIMA(0,1,1) course of. In part 3, we are going to clarify how Granger and Newbold (1974) describe the emergence of nonsense regressions, with examples illustrated in part 4. Lastly, we’ll present learn how to keep away from spurious regressions when working with time collection information.

2. Easy presentation of a Random Stroll and ARIMA(0,1,1) Course of

2.1 Random Stroll

Let 𝐗ₜ be a time collection. We are saying that 𝐗ₜ follows a random stroll if its illustration is given by:

𝐗ₜ = 𝐗ₜ₋₁ + 𝜖ₜ. (1)

The place 𝜖ₜ is a white noise. It may be written as a sum of white noise, a helpful type for simulation. It’s a non-stationary time collection as a result of its variance is dependent upon the time t.

2.2 ARIMA(0,1,1) Course of

The ARIMA(0,1,1) course of is given by:

𝐗ₜ = 𝐗ₜ₋₁ + 𝜖ₜ − 𝜃 𝜖ₜ₋₁. (2)

the place 𝜖ₜ is a white noise. The ARIMA(0,1,1) course of is non-stationary. It may be written as a sum of an impartial random stroll and white noise:

𝐗ₜ = 𝐗₀ + random stroll + white noise. (3) This way is beneficial for simulation.

These non-stationary collection are sometimes employed as benchmarks towards which the forecasting efficiency of different fashions is judged.

3. Random stroll can result in Nonsense Regression

First, let’s recall the Linear Regression mannequin. The linear regression mannequin is given by:

𝐘 = 𝐗𝛽 + 𝜖. (4)

The place 𝐘 is a T × 1 vector of the dependent variable, 𝛽 is a Ok × 1 vector of the coefficients, 𝐗 is a T × Ok matrix of the impartial variables containing a column of ones and (Ok−1) columns with T observations on every of the (Ok−1) impartial variables, that are stochastic however distributed independently of the T × 1 vector of the errors 𝜖. It’s typically assumed that:

𝐄(𝜖) = 0, (5)

and

𝐄(𝜖𝜖′) = 𝜎²𝐈. (6)

the place 𝐈 is the identification matrix.

A check of the contribution of impartial variables to the reason of the dependent variable is the F-test. The null speculation of the check is given by:

𝐇₀: 𝛽₁ = 𝛽₂ = ⋯ = 𝛽ₖ₋₁ = 0, (7)

And the statistic of the check is given by:

𝐅 = (𝐑² / (𝐊−1)) / ((1−𝐑²) / (𝐓−𝐊)). (8)

the place 𝐑² is the coefficient of dedication.

If we need to assemble the statistic of the check, let’s assume that the null speculation is true, and one tries to suit a regression of the shape (Equation 4) to the degrees of an financial time collection. Suppose subsequent that these collection usually are not stationary or are extremely autocorrelated. In such a state of affairs, the check process is invalid since 𝐅 in (Equation 8) shouldn’t be distributed as an F-distribution beneath the null speculation (Equation 7). In truth, beneath the null speculation, the errors or residuals from (Equation 4) are given by:

𝜖ₜ = 𝐘ₜ − 𝐗𝛽₀ ; t = 1, 2, …, T. (9)

And can have the identical autocorrelation construction as the unique collection 𝐘.

Some thought of the distribution drawback can come up within the state of affairs when:

𝐘ₜ = 𝛽₀ + 𝐗ₜ𝛽₁ + 𝜖ₜ. (10)

The place 𝐘ₜ and 𝐗ₜ comply with impartial first-order autoregressive processes:

𝐘ₜ = 𝜌 𝐘ₜ₋₁ + 𝜂ₜ, and 𝐗ₜ = 𝜌* 𝐗ₜ₋₁ + 𝜈ₜ. (11)

The place 𝜂ₜ and 𝜈ₜ are white noise.

We all know that on this case, 𝐑² is the sq. of the correlation between 𝐘ₜ and 𝐗ₜ. They use Kendall’s consequence from the article Knowles (1954), which expresses the variance of 𝐑:

𝐕𝐚𝐫(𝐑) = (1/T)* (1 + 𝜌𝜌*) / (1 − 𝜌𝜌*). (12)

Since 𝐑 is constrained to lie between -1 and 1, if its variance is larger than 1/3, the distribution of 𝐑 can not have a mode at 0. This suggests that 𝜌𝜌* > (T−1) / (T+1).

Thus, for instance, if T = 20 and 𝜌 = 𝜌*, a distribution that isn’t unimodal at 0 will probably be obtained if 𝜌 > 0.86, and if 𝜌 = 0.9, 𝐕𝐚𝐫(𝐑) = 0.47. So the 𝐄(𝐑²) will probably be near 0.47.

It has been proven that when 𝜌 is near 1, 𝐑² may be very excessive, suggesting a powerful relationship between 𝐘ₜ and 𝐗ₜ. Nevertheless, in actuality, the 2 collection are utterly impartial. When 𝜌 is close to 1, each collection behave like random walks or near-random walks. On prime of that, each collection are extremely autocorrelated, which causes the residuals from the regression to even be strongly autocorrelated. Because of this, the Durbin-Watson statistic 𝐝 will probably be very low.

For this reason a excessive 𝐑² on this context ought to by no means be taken as proof of a real relationship between the 2 collection.

To discover the potential of acquiring a spurious regression when regressing two impartial random walks, a collection of simulations proposed by Granger and Newbold (1974) will probably be performed within the subsequent part.

4. Simulation outcomes utilizing Python.

On this part, we are going to present utilizing simulations that utilizing the regression mannequin with impartial random walks bias the estimation of the coefficients and the speculation checks of the coefficients are invalid. The Python code that can produce the outcomes of the simulation will probably be offered in part 6.

A regression equation proposed by Granger and Newbold (1974) is given by:

𝐘ₜ = 𝛽₀ + 𝐗ₜ𝛽₁ + 𝜖ₜ

The place 𝐘ₜ and 𝐗ₜ had been generated as impartial random walks, every of size 50. The values 𝐒 = |𝛽̂₁| / √(𝐒𝐄̂(𝛽̂₁)), representing the statistic for testing the importance of 𝛽₁, for 100 simulations will probably be reported within the desk under.

The null speculation of no relationship between 𝐘ₜ and 𝐗ₜ is rejected on the 5% stage if 𝐒 > 2. This desk exhibits that the null speculation (𝛽 = 0) is wrongly rejected in a couple of quarter (71 occasions) of all instances. That is awkward as a result of the 2 variables are impartial random walks, that means there’s no precise relationship. Let’s break down why this occurs.

If 𝛽̂₁ / 𝐒𝐄̂ follows a 𝐍(0,1), the anticipated worth of 𝐒, its absolute worth, must be √2 / π ≈ 0.8 (√2/π is the imply of absolutely the worth of a typical regular distribution). Nevertheless, the simulation outcomes present a median of 4.59, that means the estimated 𝐒 is underestimated by an element of:

4.59 / 0.8 = 5.7

In classical statistics, we normally use a t-test threshold of round 2 to verify the importance of a coefficient. Nevertheless, these outcomes present that, on this case, you would wish to make use of a threshold of 11.4 to correctly check for significance:

2 × (4.59 / 0.8) = 11.4

Interpretation: We’ve simply proven that together with variables that don’t belong within the mannequin — particularly random walks — can result in utterly invalid significance checks for the coefficients.

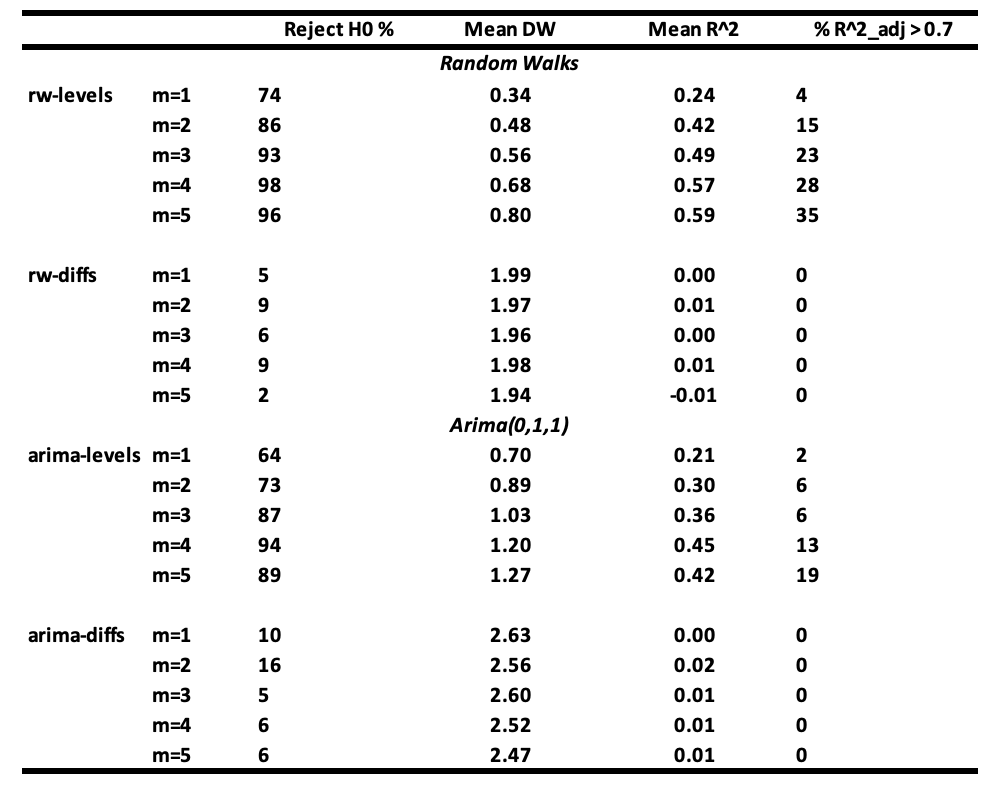

To make their simulations even clearer, Granger and Newbold (1974) ran a collection of regressions utilizing variables that comply with both a random stroll or an ARIMA(0,1,1) course of.

Right here is how they arrange their simulations:

They regressed a dependent collection 𝐘ₜ on m collection 𝐗ⱼ,ₜ (with j = 1, 2, …, m), various m from 1 to five. The dependent collection 𝐘ₜ and the impartial collection 𝐗ⱼ,ₜ comply with the identical varieties of processes, they usually examined 4 instances:

- Case 1 (Ranges): 𝐘ₜ and 𝐗ⱼ,ₜ comply with random walks.

- Case 2 (Variations): They use the primary variations of the random walks, that are stationary.

- Case 3 (Ranges): 𝐘ₜ and 𝐗ⱼ,ₜ comply with ARIMA(0,1,1).

- Case 4 (Variations): They use the primary variations of the earlier ARIMA(0,1,1) processes, that are stationary.

Every collection has a size of fifty observations, they usually ran 100 simulations for every case.

All error phrases are distributed as 𝐍(0,1), and the ARIMA(0,1,1) collection are derived because the sum of the random stroll and impartial white noise. The simulation outcomes, based mostly on 100 replications with collection of size 50, are summarized within the subsequent desk.

Interpretation of the outcomes :

- It’s seen that the chance of not rejecting the null speculation of no relationship between 𝐘ₜ and 𝐗ⱼ,ₜ turns into very small when m ≥ 3 when regressions are made with random stroll collection (rw-levels). The 𝐑² and the imply Durbin-Watson improve. Related outcomes are obtained when the regressions are made with ARIMA(0,1,1) collection (arima-levels).

- When white noise collection (rw-diffs) are used, classical regression evaluation is legitimate because the error collection will probably be white noise and least squares will probably be environment friendly.

- Nevertheless, when the regressions are made with the variations of ARIMA(0,1,1) collection (arima-diffs) or first-order transferring common collection MA(1) course of, the null speculation is rejected, on common:

(10 + 16 + 5 + 6 + 6) / 5 = 8.6

which is larger than 5% of the time.

In case your variables are random walks or near them, and also you embody pointless variables in your regression, you’ll typically get fallacious outcomes. Excessive 𝐑² and low Durbin-Watson values don’t verify a real relationship however as an alternative point out a probable spurious one.

5. The way to keep away from spurious regression in time collection

It’s actually arduous to provide you with a whole listing of the way to keep away from spurious regressions. Nevertheless, there are a number of good practices you’ll be able to comply with to decrease the chance as a lot as doable.

If one performs a regression evaluation with time collection information and finds that the residuals are strongly autocorrelated, there’s a major problem on the subject of deciphering the coefficients of the equation. To verify for autocorrelation within the residuals, one can use the Durbin-Watson check or the Portmanteau check.

Primarily based on the examine above, we will conclude that if a regression evaluation carried out with economical variables produces strongly autocorrelated residuals, that means a low Durbin-Watson statistic, then the outcomes of the evaluation are more likely to be spurious, regardless of the worth of the coefficient of dedication R² noticed.

In such instances, it is very important perceive the place the mis-specification comes from. In keeping with the literature, misspecification normally falls into three classes : (i) the omission of a related variable, (ii) the inclusion of an irrelevant variable, or (iii) autocorrelation of the errors. More often than not, mis-specification comes from a mixture of these three sources.

To keep away from spurious regression in a time collection, a number of suggestions may be made:

- The primary advice is to pick out the fitting macroeconomic variables which are more likely to clarify the dependent variable. This may be carried out by reviewing the literature or consulting consultants within the area.

- The second advice is to stationarize the collection by taking first variations. Usually, the primary variations of macroeconomic variables are stationary and nonetheless straightforward to interpret. For macroeconomic information, it’s strongly beneficial to distinguish the collection as soon as to scale back the autocorrelation of the residuals, particularly when the pattern dimension is small. There’s certainly generally robust serial correlation noticed in these variables. A easy calculation exhibits that the primary variations will nearly all the time have a lot smaller serial correlations than the unique collection.

- The third advice is to make use of the Field-Jenkins methodology to mannequin every macroeconomic variable individually after which seek for relationships between the collection by relating the residuals from every particular person mannequin. The thought right here is that the Field-Jenkins course of extracts the defined a part of the collection, leaving the residuals, which include solely what can’t be defined by the collection’ personal previous conduct. This makes it simpler to verify whether or not these unexplained elements (residuals) are associated throughout variables.

6. Conclusion

Many econometrics textbooks warn about specification errors in regression fashions, however the issue nonetheless exhibits up in lots of revealed papers. Granger and Newbold (1974) highlighted the chance of spurious regressions, the place you get a excessive paired with very low Durbin-Watson statistics.

Utilizing Python simulations, we confirmed a number of the essential causes of those spurious regressions, particularly together with variables that don’t belong within the mannequin and are extremely autocorrelated. We additionally demonstrated how these points can utterly distort speculation checks on the coefficients.

Hopefully, this submit will assist scale back the chance of spurious regressions in future econometric analyses.

7. Appendice: Python code for simulation.

#####################################################Simulation Code for desk 1 #####################################################

import numpy as np

import pandas as pd

import statsmodels.api as sm

import matplotlib.pyplot as plt

np.random.seed(123)

M = 100

n = 50

S = np.zeros(M)

for i in vary(M):

#---------------------------------------------------------------

# Generate the information

#---------------------------------------------------------------

espilon_y = np.random.regular(0, 1, n)

espilon_x = np.random.regular(0, 1, n)

Y = np.cumsum(espilon_y)

X = np.cumsum(espilon_x)

#---------------------------------------------------------------

# Match the mannequin

#---------------------------------------------------------------

X = sm.add_constant(X)

mannequin = sm.OLS(Y, X).match()

#---------------------------------------------------------------

# Compute the statistic

#------------------------------------------------------

S[i] = np.abs(mannequin.params[1])/mannequin.bse[1]

#------------------------------------------------------

# Most worth of S

#------------------------------------------------------

S_max = int(np.ceil(max(S)))

#------------------------------------------------------

# Create bins

#------------------------------------------------------

bins = np.arange(0, S_max + 2, 1)

#------------------------------------------------------

# Compute the histogram

#------------------------------------------------------

frequency, bin_edges = np.histogram(S, bins=bins)

#------------------------------------------------------

# Create a dataframe

#------------------------------------------------------

df = pd.DataFrame({

"S Interval": [f"{int(bin_edges[i])}-{int(bin_edges[i+1])}" for i in vary(len(bin_edges)-1)],

"Frequency": frequency

})

print(df)

print(np.imply(S))

#####################################################Simulation Code for desk 2 #####################################################

import numpy as np

import pandas as pd

import statsmodels.api as sm

from statsmodels.stats.stattools import durbin_watson

from tabulate import tabulate

np.random.seed(1) # Pour rendre les résultats reproductibles

#------------------------------------------------------

# Definition of capabilities

#------------------------------------------------------

def generate_random_walk(T):

"""

Génère une série de longueur T suivant un random stroll :

Y_t = Y_{t-1} + e_t,

où e_t ~ N(0,1).

"""

e = np.random.regular(0, 1, dimension=T)

return np.cumsum(e)

def generate_arima_0_1_1(T):

"""

Génère un ARIMA(0,1,1) selon la méthode de Granger & Newbold :

la série est obtenue en additionnant une marche aléatoire et un bruit blanc indépendant.

"""

rw = generate_random_walk(T)

wn = np.random.regular(0, 1, dimension=T)

return rw + wn

def distinction(collection):

"""

Calcule la différence première d'une série unidimensionnelle.

Retourne une série de longueur T-1.

"""

return np.diff(collection)

#------------------------------------------------------

# Paramètres

#------------------------------------------------------

T = 50 # longueur de chaque série

n_sims = 100 # nombre de simulations Monte Carlo

alpha = 0.05 # seuil de significativité

#------------------------------------------------------

# Definition of operate for simulation

#------------------------------------------------------

def run_simulation_case(case_name, m_values=[1,2,3,4,5]):

"""

case_name : un identifiant pour le sort de génération :

- 'rw-levels' : random stroll (ranges)

- 'rw-diffs' : variations of RW (white noise)

- 'arima-levels' : ARIMA(0,1,1) en niveaux

- 'arima-diffs' : différences d'un ARIMA(0,1,1) => MA(1)

m_values : liste du nombre de régresseurs.

Retourne un DataFrame avec pour chaque m :

- % de rejets de H0

- Durbin-Watson moyen

- R^2_adj moyen

- % de R^2 > 0.1

"""

outcomes = []

for m in m_values:

count_reject = 0

dw_list = []

r2_adjusted_list = []

for _ in vary(n_sims):

#--------------------------------------

# 1) Era of independents de Y_t and X_{j,t}.

#----------------------------------------

if case_name == 'rw-levels':

Y = generate_random_walk(T)

Xs = [generate_random_walk(T) for __ in range(m)]

elif case_name == 'rw-diffs':

# Y et X sont les différences d'un RW, i.e. ~ white noise

Y_rw = generate_random_walk(T)

Y = distinction(Y_rw)

Xs = []

for __ in vary(m):

X_rw = generate_random_walk(T)

Xs.append(distinction(X_rw))

# NB : maintenant Y et Xs ont longueur T-1

# => ajuster T_effectif = T-1

# => on prendra T_effectif factors pour la régression

elif case_name == 'arima-levels':

Y = generate_arima_0_1_1(T)

Xs = [generate_arima_0_1_1(T) for __ in range(m)]

elif case_name == 'arima-diffs':

# Différences d'un ARIMA(0,1,1) => MA(1)

Y_arima = generate_arima_0_1_1(T)

Y = distinction(Y_arima)

Xs = []

for __ in vary(m):

X_arima = generate_arima_0_1_1(T)

Xs.append(distinction(X_arima))

# 2) Prépare les données pour la régression

# Selon le cas, la longueur est T ou T-1

if case_name in ['rw-levels','arima-levels']:

Y_reg = Y

X_reg = np.column_stack(Xs) if m>0 else np.array([])

else:

# dans les cas de différences, la longueur est T-1

Y_reg = Y

X_reg = np.column_stack(Xs) if m>0 else np.array([])

# 3) Régression OLS

X_with_const = sm.add_constant(X_reg) # Ajout de l'ordonnée à l'origine

mannequin = sm.OLS(Y_reg, X_with_const).match()

# 4) Check world F : H0 : tous les beta_j = 0

# On regarde si p-value < alpha

if mannequin.f_pvalue shouldn't be None and mannequin.f_pvalue < alpha:

count_reject += 1

# 5) R^2, Durbin-Watson

r2_adjusted_list.append(mannequin.rsquared_adj)

dw_list.append(durbin_watson(mannequin.resid))

# Statistiques sur n_sims répétitions

reject_percent = 100 * count_reject / n_sims

dw_mean = np.imply(dw_list)

r2_mean = np.imply(r2_adjusted_list)

r2_above_0_7_percent = 100 * np.imply(np.array(r2_adjusted_list) > 0.7)

outcomes.append({

'm': m,

'Reject %': reject_percent,

'Imply DW': dw_mean,

'Imply R^2': r2_mean,

'% R^2_adj>0.7': r2_above_0_7_percent

})

return pd.DataFrame(outcomes)

#------------------------------------------------------

# Software of the simulation

#------------------------------------------------------

instances = ['rw-levels', 'rw-diffs', 'arima-levels', 'arima-diffs']

all_results = {}

for c in instances:

df_res = run_simulation_case(c, m_values=[1,2,3,4,5])

all_results[c] = df_res

#------------------------------------------------------

# Retailer information in desk

#------------------------------------------------------

for case, df_res in all_results.gadgets():

print(f"nn{case}")

print(tabulate(df_res, headers='keys', tablefmt='fancy_grid'))

References

- Granger, Clive WJ, and Paul Newbold. 1974. “Spurious Regressions in Econometrics.” Journal of Econometrics 2 (2): 111–20.

- Knowles, EAG. 1954. “Workouts in Theoretical Statistics.” Oxford College Press.